Renault is stepping up its transition to electric vehicles with a well-structured product offensive for 2026, in line with a strategy initiated several years ago. The French brand, with its strong European heritage, intends to reconfirm its legitimacy on the EV scene while responding to the growing pressure from global and Chinese players.

source : Renault

A year 2026 structured around two key areas

The year 2026, which has just begun, is synonymous for Renault with the launch of several new 100% electric vehicles covering both the urban segment and commercial vehicles:

The return of the iconic Twingo E-Tech electric. The small city car is being reborn in a 100% electric version with a clear ambition: to offer an EV that is affordable at under €20,000 before subsidies, a rarity in the A segment in Europe. The city car will be produced from early 2026 at the Novo Mesto plant in Slovenia, with a WLTP range of around 260 km and modern features (connectivity, fast charging, driver assistance functions). The idea behind the French brand is to meet everyday urban needs.

source : Renault

The other Renault vehicle to see the light of day is the Trafic E-Tech / FlexEVan on the electric LCV front. With this innovation, Renault is extending its range with 100% electric vans scheduled for 2026, designed for professional fleets and urban use. Based on the group’s latest EV platforms, these vans will incorporate advanced technologies and a software-defined vehicle configuration to optimise fleet management and day-to-day operations.

source : Renault

Market access facilitated by increased aid

Renault isn’t just betting on its vehicles: it’s also focusing on affordability. In 2026, the French government has renewed the enhanced CEE scheme. Thanks to the entry price of the Twingo E-Tech electric combined with various “Classic” and “Helping Hand” bonuses, the price of the latter will be reduced to around €13,750 for households on the lowest incomes. The brand’s commercial vehicles will also be eligible for various incentives from the start of the year.

A long-term electricity strategy

The products 2026 offensive is part of a longer-term strategic roadmap, supported by the Renaulution plan, which aims to give Renault a strong position in European and global electromobility.

ElectriCity & batteries in Europe Renault has consolidated its industrial capacity around the ElectriCity cluster in northern France, bringing together plants in Douai, Maubeuge and Ruitz to optimise EV production. Nearby, an AESC gigafactory in Douai produces competitive low-carbon batteries, with the aim of achieving a capacity of up to 24 GWh by 2030. A second Verkor site is planned to produce around 10 GWh of batteries from 2026, strengthening the Group’s industrial autonomy.

source : Renault

In-house technologies and platforms Renault is also pushing ahead with the development of proprietary electric motors, integrated power electronics solutions and dedicated platform architectures such as CMF-BEV to reduce production costs and improve the efficiency and competitiveness of its EV models.

Electric vehicle mix targets The Group’s ambition is to have a sales mix with more than 65% electric and electrified vehicles by 2025, with a progression towards a predominant BEV mix by 2030, in line with European emission reduction standards.

A European perspective: Renault and the competition

In Europe, Renault’s efforts must be seen in the context of its main competitors:

Volkswagen Group, with a vast ID range and projects such as the ID.Polo, scheduled for 2026, remains a heavyweight in the European EV market. VW is counting on high volumes and a strong presence in all consumer segments.

Stellantis (Peugeot, Citroën, Opel, etc.) is pursuing a more ‘mixed’ strategy, combining electric and hybrid technologies while targeting affordable light commercial vehicles and city cars.

Chinese players such as BYD are pushing European players to review their pricing and innovation strategies, particularly in the urban/very affordable segments, while at the same time creating partnerships (e.g. Renault-Ford alliance announced to develop small EVs from 2028).

Renault stands out for its product strategy covering city cars, SUVs and electric light commercial vehicles, and for its strong industrial integration in Europe, which gives it an advantage in the race for electrification on the Old Continent.

Conclusion

With 2026 as its pivotal year, Renault is setting its EV strategy on a clear course: a structured product offensive, easier economic access, strengthened industrial capacities and assertive European ambitions. With the Twingo E-Tech electric city car designed to make electromobility accessible to all, and LCVs to meet the needs of professionals, Renault is positioning itself as a major European player, ready to take on its rivals while continuing the profound transformation that has already been underway for several years.

The UK is approaching the end of 2025 as one of Europe’s most advanced markets for electromobility, with a high share of the electric market, an ever-growing recharging infrastructure and a policy framework now structured around the ZEV mandate, but still with real obstacles in terms of purchase costs, future taxation and regional disparities.

Market and sales volumes

For once, the UK market accelerated in 2025. Between January and the end of November 2025, no fewer than 426,000 100% electric cars (BEVs) were registered in the UK. This significant figure represents an increase of 26% compared with 2024, giving EVs a 22.7% share of the new car market. Number of cars on the road: around 1.75 million 100% electric cars, or 5.2% of the 34 million cars on the road in the UK.

In terms of hybrid technology, 208,000 PHEVs were sold over the same period last year, for a market share of just over 11%. As for HEVs, 260,000 new vehicles were registered, representing a market share of 14.0%.

For electric light commercial vehicles (LCVs), although public data remains patchy for the year 2025 as a whole, monthly statistics from the SMMT (Society of Motor Manufacturers and Traders) show a sharp rise in sales of electric vans, with around 27,000 registrations to the end of November, representing an increase of almost 45% over one year.

Number of charging points and recharging network

Charging infrastructure has grown significantly since 2020, with a clear political target of 300,000 public charging points by 2030. It’s an ambitious target, but one that still seems a long way from being achieved. In fact, at the end of November 2025, the UK had more than 87,000 public charging points, with a dense but still very uneven network between regions. These solutions are spread over 44,326 separate sites and offer a total of 121,364 connectors. The average density is 127.3 chargepoints per 100,000 inhabitants, but there are wide variations, reflecting the fact that access is still very patchy. In London, for example, there are 300.8 terminals per 100,000 inhabitants, compared with 38.6 in Northern Ireland.

source : circontrol

In 2025, 13,469 chargepoints were added across the country, including 6,220 slow chargepoints and 3,358 fast or ultra-fast chargepoints. Although this figure is significant and represents an annual increase of around 18%, it is the smallest increase since 2022.

The major private operators now dominate the fast-grid landscape: InstaVolt (2,169 fast/ultrarapid kiosks), Tesla (2,026) and Osprey (1,351) make up the top three by the end of 2025.

source: Instavolt

Public policy, aid and taxation

With the aim of developing this market as effectively as possible and enabling EVs to become more widely available, legislation and incentives have been introduced. The UK framework is based on two pillars: a tight regulatory mandate for manufacturers (ZEV mandate) and targeted subsidies, notably relaunched in 2025 with a new “plug-in grant”.

ZEV mandate: the regulatory framework imposes on manufacturers a target of 28% sales of 100% electric vehicles by 2025, with a gradual trajectory leading to the end of sales of new combustion engine cars within the decade. By autumn 2025, the market share of BEVs was around 26%, slightly below this overall target, even though the scheme provides flexibility mechanisms for manufacturers.

Plug-in Grant 2025: a new purchase aid for electric cars was relaunched in the summer of 2025, with a twelve-month extension announced as part of the budget presented by Chancellor Rachel Reeves. The grant is deducted directly from the purchase price at the dealership.

Additional support: the scheme is complemented by OZEV grants for the installation of home and business charging points, as well as funding programmes dedicated to local authorities, in particular the LEVI fund for the local deployment of infrastructure.

Taxation: the planned end of the exemption from Vehicle Excise Duty (VED) for electric vehicles is fuelling questions about the economic attractiveness of electric vehicles in the medium term, particularly for households.

source: Automobile propre

Top-selling models and industry players

In terms of sales and best-selling models, the market is still dominated by the major global generalists rather than by national manufacturers, but the UK ecosystem has specialised in recharging and services.

Best-selling vehicles: in 2025, the UK electric car market continues to be dominated by the Tesla Model Y, which remains the most popular BEV model, closely followed by the MG4 EV and other electric SUVs and saloons such as the Tesla Model 3, Volkswagen ID.4 or Volvo EX30.

source : MG

Plug-in hybrids (PHEVs) are making rapid progress, with models such as the BYD Seal U DM-i among the most popular in this segment, which is particularly popular with fleets and commuters.

Conventional hybrids (HEV) continue to have a strong presence in the general market, notably with the Toyota Corolla Hybrid and the Ford Puma Hybrid, which combine affordability with low fuel consumption.

The range of electric and hybrid cars available in the UK now exceeds 150 models, with an average price of around £46,000, while the entry-level segment is expanding rapidly, with vehicles available for under £30,000, led by the Dacia Spring.

The UK has a fast-growing ecosystem of companies involved in electric mobility.

Charging operators: InstaVolt, Osprey, BP Pulse (BP), Shell Recharge UK and others are developing networks of fast charging points and high-power hubs throughout the country, with a particularly dense network in the south and around London.

Services and leasing: many local players – rental companies, brokers and leasing platforms – specialise in electric fleet management and recharging solutions for individuals and businesses.

Production and R&D: the UK is home to several battery and electrified vehicle production sites operated by foreign groups, as well as gigafactory projects, although the sector remains less integrated than in Germany or China.

Brakes and friction points

Despite solid figures, the transition to electromobility in the UK remains gradual, with a number of structural obstacles:

Purchase cost: the average price of a new electric vehicle is around £46,000, driven in part by premium models such as Tesla and Audi. The entry-level range is growing, with models under £30,000 (MG4, BYD Dolphin, Citroën ë-C3), but is still a minority in terms of volume. Public subsidies, such as the Plug-in Grant and OZEV subsidies, partially reduce the additional cost compared with combustion vehicles.

Uneven infrastructure: the major conurbations in the south and London benefit from a well-developed network of charging stations, but there are still “white zones” in the north, in Northern Ireland and in certain rural areas, particularly for fast and ultra-fast charging stations.

Tax uncertainties: the gradual end of the exemption from VED (road tax) for EVs and the prospect of a kilometre tax by 2028 are fuelling a degree of caution among households.

Car culture and usage: many drivers remain attached to combustion-powered vehicles for long journeys. Concerns remain about the real range, residual value and long-term reliability of batteries, sometimes putting the brakes on the decision to buy.

To sum up, the UK now ticks most of the boxes for a mature EV market: high market share, fleet in excess of 5%, dense recharging network and ambitious policy framework. But the next step, that of mass adoption beyond the ‘early adopters’, will depend on the ability to reduce the entry ticket, fill the infrastructure gaps and stabilise the fiscal framework.

The Ferrari Testarossa, icon of the 1980s, continues to make its mark on automotive history, but now from a legal and strategic rather than a technical perspective. In July 2025, the Court of Justice of the European Union (CJEU) confirmed that Ferrari retains its rights to the ‘Testarossa’ trademark, stressing that use of the name, even on second-hand vehicles, spare parts or derivative products, remains sufficiently active to justify its protection. This decision reflects the cultural and commercial importance of the name in the minds of the European public.

source : motorcargallery

A historic name, a bridge to the future

While no new Testarossa has been produced, Ferrari is integrating the concept of heritage into its modern strategy. The brand continues to develop its hybrid and electric powertrains, with PHEV models and 100% electric vehicles planned for the coming years. The strategic plan presented at the Ferrari Capital Markets Day 2025 confirms the brand’s ambition to maintain the prestige of its supercars while gradually adopting cleaner technologies.

credit: Bloomberg

Cultural heritage as a strategic lever

The Testarossa name, which has been part of the collective imagination since 1984, remains a powerful symbol of Ferrari’s history. The CJEU’s decision not only protects the brand’s rights, but also strengthens Ferrari’s ability to exploit this heritage in derivative products, collections and special editions. This heritage enables the brand to anchor its future hybrid or electric models in a cultural continuity that is recognised and valued by collectors and enthusiasts.

source : motorcargallery

Ferrari and the technological transition

In its roadmap to 2030, Ferrari is planning a ramp-up in hybrid models, followed by the introduction of its first 100% electric car scheduled for 2027-2028. This transition is being made gradually, while maintaining the performance and driving experience for which the brand is renowned, and meeting global environmental and regulatory imperatives.

source : spectrum

Conclusion: a protected name and an assertive strategy

The Testarossa is no longer just an iconic supercar: it has become a strategic tool, linking Ferrari’s cultural heritage with its technological ambitions. By legally protecting this name and preparing its transition to hybrid and electric vehicles, Ferrari is asserting its desire to combine passion, innovation and the long-term future of the brand.

In the UK, sales of electric vehicles continue to rise, supported by the ZEV Mandate quotas, but the roll-out of public charging points is struggling to keep pace. While the total number of charging points is growing every year, the slower pace of installation and regional disparities raise questions about the network’s ability to keep pace with the growth in EV use, particularly for private customers and long-distance journeys.

source: Phil Wilkinson/Alamy

A network that continues to grow… but at a slower pace

In the UK, the roll-out of electric vehicle (EV) charging points is still progressing in 2025, but at a slower rate than the adoption of vehicles themselves. According to the latest data from The Guardian, the pace of installation has slowed markedly this year, with just 13,500 new public chargers installed between the end of 2024 and the end of November 2025, compared with stronger growth in previous years. This brings the total public network to around 87,200 charging points by the end of November 2025, an annual increase of around 18%, the lowest since 2022.

Strong growth in EV sales

In the UK, electric vehicles account for a growing share of the market. In fact, according to registration statistics, EVs accounted for almost 23% of new car sales in the first 11 months of 2025, compared with around 19% in the same period the previous year. A fine progression, then, for this emerging market, which is becoming increasingly important.

European manufacturers are leading the charge: BMW has 34.4% of BEV sales, Mercedes-Benz 36.6%. The Tesla Model Y (18,310 units) and Model 3 (16,605) dominate the sales rankings for the first nine months.

source : BMW

Fast infrastructure still inadequate

It’s true that the roll-out of charging points is slowing down. But the market is growing. According to Zapmap, there were already more than 87,200 charging points on the network at the end of October 2025, an increase of around 23% over one year. While there has been an increase in the number of so-called fast and ultra-fast chargepoints, which are essential for long-distance journeys, they remain a fraction of the total, still limiting the ability to make long electric journeys, and so British drivers are still not completely convinced about adopting an EV.

According to the latest data from The Guardian, the pace of installation has slowed markedly this year, with just 13,500 new public chargers installed between the end of 2024 and the end of November 2025, compared with stronger growth in previous years. This brings the total public network to around 87,200 charging points by the end of November 2025, an annual increase of less than 20%, the lowest since 2022.

Major regional disparities

The geographical disparities are still glaring: some urban areas, such as London, are home to 22,211 public pay stations (250 per 100,000 inhabitants), 2.3 times the national average of 108 per 100,000.

source : motor 1

Conversely, regions such as Northern Ireland have a ceiling of 36 charging points per 100,000 inhabitants. On motorways, only a third of service areas have at least six ultra-fast chargers.

These differences may influence consumer confidence and limit the adoption of EVs outside major cities.

The role of the ZEV Mandate

In this context, public policy plays a key role. The Zero Emission Vehicle (ZEV) Mandate, designed to push manufacturers to sell more zero-emission vehicles, continues to support the growth of EV sales in the UK, although the implementation and political signals around this policy may create some uncertainty for infrastructure investors.

The introduction in July 2025 of theElectric Car Grant, offering up to £3,750 cashback on new cars under £37,000, has undeniably boosted the market. More than 40 models are now eligible, considerably widening the choice for buyers.

A crossroads for electric mobility

The UK is at a pivotal point in its transition: EV sales continue to grow, but the public network needs to keep pace to ensure continued uptake, particularly for consumers and in rural areas. The next few months will be crucial in determining whether the roll-out of charging points can accelerate and sustainably support the rise of electric cars.

As 2025 draws to a close, French road safety continues to face a number of challenges. With the number of deaths on the rise in November and legislation tightened to an all-time high since 29 December 2025, the authorities are stepping up measures to reduce the number of road accidents. The question is: can EVs help to reduce the risks?

source: connexion France

November 2025: a worrying upturn in road deaths

According to the latest figures from the Observatoire national interministériel de la sécurité routière (ONISR), 270 people were killed on the roads of mainland France in November 2025, compared with 266 in November 2024, an increase of around 2% over one year. In addition to these figures, there were 13 deaths in the French overseas departments and territories, bringing the national total for November to 283.

This increase puts an end to the fall in fatalities observed in October, and confirms worrying trends for several categories of road user. Young people under the age of 24 are particularly hard hit, with an increase in the number of deaths in this age group. Pedestrian fatalities were also up over the month, while those aged over 65 were down on the previous year. Geographically, fatalities fell in built-up areas but rose on roads outside built-up areas and on motorways.

In addition, over a 12-month rolling trend, road deaths are still on the rise, driven in particular by an increase in deaths among users of motorised personal mobility devices (PMDs), such as scooters.

In terms of serious injuries, November saw a slight fall, with an estimated 1,213 cases in mainland France, compared with 1,242 in November 2024, again according to the ONISR.

Speeding too fast becomes an offence

Faced with this situation, the authorities have decided to significantly tighten the legal framework. Since 29 December 2025, any speeding of at least 50 km/h over the authorised limit has been classified as an offence, rather than a simple fifth-class fine.

source: policechiefmagazine

According to the press release from the French road safety authority, this measure has come into force following the publication of a decree in application of the law of 9 July 2025 creating road homicide and aimed at combating road violence and reinforcing the judicial response to the most dangerous driving behaviours.

From now on, offenders will face stiffer penalties:

a penalty of up to three months’ imprisonment ;

a maximum fine of €3,750;

a criminal record ;

suspension of driving licence for up to three years;

possible confiscation of the vehicle;

and the obligation to complete a road safety awareness course.

Until now, very excessive speeding was only punished by a fine, except in the case of a repeat offence.

The EV is a safety asset

In this context of the fight against road accidents, electric vehicles (EVs) have safety features that deserve to be highlighted. Several international studies confirm that driving an EV is safer overall than driving a combustion engine vehicle.

source: beev.co

Better impact protection

EVs benefit from major structural advantages in terms of crashworthiness. Their lower centre of gravity reduces the risk of rollover, according to data from the National Highway Traffic Safety Administration (NHTSA) and the Insurance Institute for Highway Safety (IIHS). The absence of an internal combustion engine at the front of the vehicle means that deformation zones can be optimised to dissipate energy in the event of an impact, resulting in excellent crash-test performance. Many electric vehicles have been awarded a 5-star rating in euro NCAP safety tests.

A Norwegian study of more than 500,000 vehicles shows that EVs are associated with 20-30% fewer fatalities in the event of a collision, a performance attributed in part to the standard integration of advanced driving aids such as automatic emergency braking (AEB).

source: Euro NCAP

A much lower risk of fire

Fires are much rarer in electric vehicles than in combustion vehicles. In the United States, the National Transportation Safety Board reports 25 EV fires for every 100,000 vehicles sold, compared with 1,529 for internal combustion vehicles. Specialist sources such as EV FireSafe estimate that the risk of fire is up to 80 times lower for EVs, thanks to the absence of flammable liquid fuel and sophisticated battery management systems (BMS).

A few nuances to consider

Some studies, such as a Dutch study of over 14,000 vehicles, note a slight increase in minor accidents for EVs (3.2% more), possibly linked to instant acceleration or more frequent urban use. However, the same data also showed a reduction in serious head-on collisions involving EVs.

Overall, the IIHS data for 2024 confirms that EVs have fewer injuries per kilometre travelled than combustion vehicles. This trend is set to strengthen as electromobility becomes more widespread and safety technologies continue to improve.

Conclusion: using technology to enhance safety

Faced with a rise in road deaths in November 2025 and tougher legislation, the electrification of the car fleet could help to improve safety on our roads. The intrinsic characteristics of electrified vehicles make them objectively safer than internal combustion engines.

While technology will never replace the individual responsibility of drivers or the need to comply with speed limits, it can nevertheless offer valuable additional protection. Road safety remains a major challenge requiring mobilisation on all fronts.

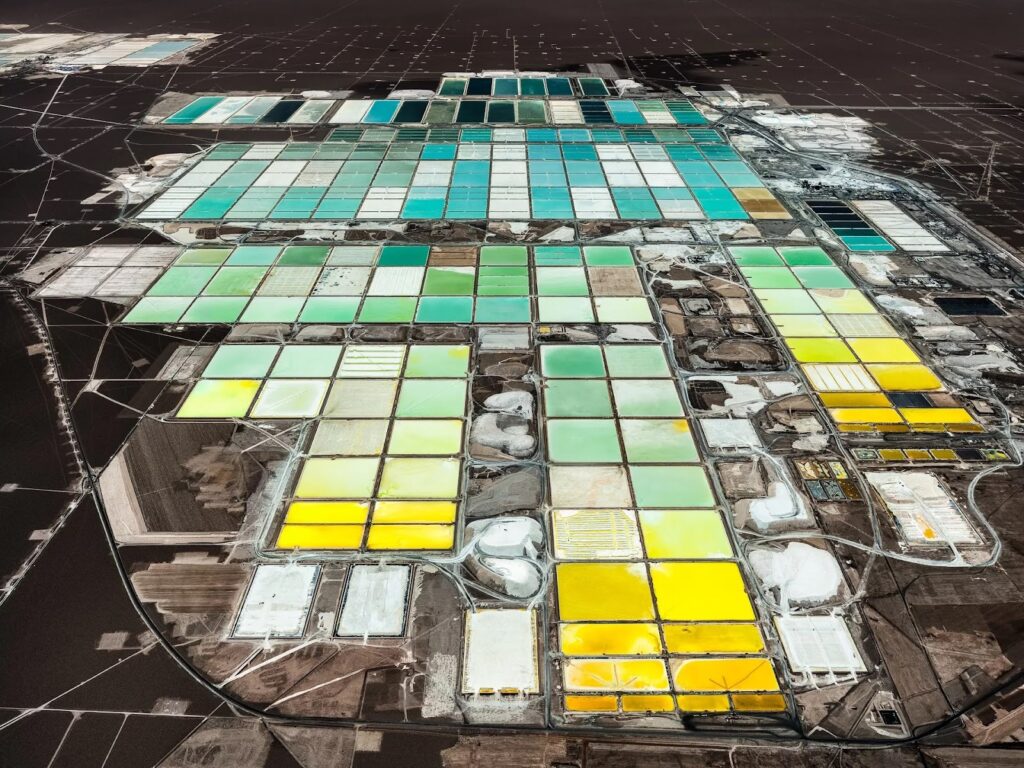

Chile has just announced the birth of a new lithium behemoth. This project reinforces the country’s strategic importance in the “lithium triangle”, but reopens the debate on the environmental footprint of salt extraction.

source: mining technology

A public-private project lasting until 2060

On 26 December 2025, the Chilean government (via the state-owned company Codelco) and the private producer SQM formalised the creation of Nova Andino Litio SpA. This joint venture will merge their assets to exploit the lithium of the Salar d’Atacama – a vast 3,000 km² salt desert in northern Chile – until 2060.

The Chilean government will capture 70% of operating margins from 2025 to 2030, then 85% from 2031, as part of the National Lithium Strategy launched in 2023. The aim is to perpetuate and even increase current production of 280-300,000 tonnes of lithium carbonate a year, consolidate Chile’s leadership (ranked 2nd in the world behind Australia) and maximise local value by strengthening public control of strategic salars.

A strategic asset for electromobility

This is good news for the battery and electric vehicle industry. This new agreement means a massive supply of lithium, with long-term contracts securing volumes for cell manufacturers and carmakers.

source: Codelco

It is occurring in Chile, which holds around 40% of the world’s reserves and accounts for almost 24% of global production. What’s more, extraction by evaporation in the Salar d’Atacama offers a major competitive advantage: costs of between $3,800 and $4,200 per tonne, compared with $5,100 to $6,000 for Australian lithium.

Extraction with a high environmental impact

The lithium extraction process at the Salar d’Atacama involves pumping a rich brine (0.2% Li) to a depth of 30-40 m, then pouring it into vast plastic-coated basins where 95% of the water evaporates naturally under the Atacama sun for 12 to 18 months. Sodium chloride and sodium carbonate are then added to obtain crude lithium carbonate (Li₂CO₃), which is dried and refined to 99.5% before being exported to EV battery cathode factories. This low-cost process consumes 2 million litres of water per tonne and puts significant pressure on groundwater.

source : Tom Hegen

Lithium extraction in the Chilean salars is polluting and consumes a lot of water. Pumping brine has already had a measurable impact on the ecosystem.

The figures speak for themselves: water levels have fallen by 30% in some areas, the flamingo population has fallen by 10% since industrialisation began, and the ground has been subsiding by 1 to 2 cm per year since 2019 in areas of intensive exploitation. According to the UN, lithium and copper extraction consume up to 65% of the water available in the Salar d’Atacama region.

source: Terre des andes

To address these problems of pollution and destruction of biodiversity, Chile’s National Strategy calls for 30% of salars to be protected by 2030 and for the development of technologies that have less impact.

The paradox of electromobility

This dossier is an uncomfortable reminder that there is no such thing as a “zero-emission car”. There are major gains in terms of use, but the upstream chain remains destructive for ultra-fragile ecosystems.

The creation of Nova Andino Litio marks a turning point in the global governance of lithium. By regaining control via a majority state-owned joint venture, Chile is sending out a clear signal: the days when multinationals were free to exploit the Chilean salars are over. From now on, it is the state that sets the rules, capturing most of the profit.

It remains to be seen whether this new direction will actually lead to better protection of ecosystems. For the time being, the pressure on water resources continues unabated. Lithium remains essential to the global energy transition, but its extraction must become cleaner.

Home charging covers around 70% of the daily needs of electric vehicle drivers, and offers them unrivalled convenience. But from next year, with the CIBRE tax credit due to expire on 31 December 2025, it’s vital to be aware of the support and solutions available to continue equipping your home at a lower cost.

CIBRE: major support until 2025

With the aim of democratising electrically powered vehicles, since 2021 the CIBRE (Crédit d’Impôt pour la Borne de Recharge Électrique – Tax Credit for Electric Charging Stations) has been introduced by the French government and has supported tens of thousands of households. In fact, in 2024 alone, this aid scheme enabled almost 47,000 households to benefit from a home charging point.

It covered up to €500 per controllable bollard installed by an IRVE professional, or up to €1,000 for two bollards per couple, depending on the installer.

To be eligible, the charging point had to be permanently fixed and controllable, and the installation had to be carried out by an IRVE professional. The homes concerned could be primary or secondary residences, completed more than two years ago and not rented out.

In addition to this tax credit, from 2023 onwards, all domestic charging points will benefit from reduced VAT of 5.5%, including reinforced Green’Up-type sockets.

source: WEG

The end of CIBRE: planning for the future

However, from January 2026, CIBRE will cease to exist. The main reasons for this are budgetary constraints and the government’s desire to rationalise tax incentives for the energy transition.

This translates into savings for a couple with two homes, which will fall from around €1,000 to €250 thanks to the reduced VAT. The cost of a typical 7.4 kW installation (terminal, installation, wiring and protection) will remain between €1,200 and €1,800 including VAT.

Remaining support for individuals

Even without the CIBRE, a number of levers remain available. For single-family homes, reduced VAT is the main tax incentive, supplemented by local grants, the amount of which varies greatly from region to region.

In the Île-de-France region, grants range from €300 to €500, with some condominiums eligible for as much as €960. In Occitanie, the regional grant is €500. In Auvergne-Rhône-Alpes, it ranges from €400 to €1,000. In some areas of the Provence-Alpes-Côte d’Azur region, the total amount of assistance can be as much as €1,500.

Advenir: a central programme for condominiums

Another area where home charging stations are useful is in condominiums and collective housing. The Advenir programme will continue to be a key tool in this area until 2027. It covers up to 50% of the costs of individual and shared charging points, with a ceiling of €600 per individual charging point and €1,660 per shared charging point.

For collective infrastructures, the subsidy is 50% up to €8,000 for 100 spaces, with a bonus for outdoor car parks and specific wiring. These grants can be combined with each other and with reduced VAT.

source: advenir

Innovative solutions from installers

To keep installations accessible, professionals in the sector are now offering intelligent controllable terminals, capable of modulating power, programming sessions via mobile application and sometimes V2G compatible.

In condominiums, plug-and-play modular solutions reduce work and costs by 30-50%. Some monthly rental packages include installation, maintenance and replacement, to limit the initial investment.

A sustainable economic advantage

These aids are useful and economical to use. Charging at home is still very competitive. At off-peak times, electricity costs €0.10 to €0.15/kWh, compared with €0.40 to €0.80/kWh at normal public charging points and up to €1/kWh at fast motorway charging points.

For a vehicle consuming 15 kWh/100 km and travelling 15,000 km a year, the annual saving could be as much as €1,000 to €1,500.

Post-CIBRE: new approaches

From 2026 onwards, reduced VAT will remain the national tax advantage, local aid will support certain single-family homes, and Advenir will continue to provide support for condominiums. Leasing and staggered payment solutions will become important levers for maintaining accessibility.

The aim remains clear: to ensure that home charging retains its central role in the electricity transition and remains accessible to as many people as possible.

In December 2025, SERMA Technologies inaugurated a new battery testing centre for electric mobility in Neuville-aux-Bois (Loiret). The 5,000 m² site is entirely dedicated to safety, performance and reliability testing of lithium-ion battery cells, modules and packs.

source : Serma

The project is supported by the France 2030 programme and the Green Fund, and is part of the national strategy to strengthen France’s industrial capacity in the field of electromobility. It complements the Group’s existing facilities at Martillac (Gironde) and Lardy (Essonne).

Comprehensive tests to validate safety

The Loiret centre is responsible for carrying out a wide range of tests to assess the behaviour of batteries in extreme conditions. SERMA’s tests include the following:

thermal tests (runaway, propagation, temperature rise),

and environmental tests (immersion, humidity, thermal variations).

source : Serma

These highly regulated procedures are carried out in accordance with UN 38.3, ECE R100 and IEC 62660 standards, which are used to qualify and approve batteries for EVs.

The facilities include secure, confined areas equipped with detection, fire containment and smoke treatment systems to neutralise any incident during destructive testing.

An asset for the French battery industry

This new centre strengthens the testing and validation activities of SERMA Technologies, which specialises in the electrical, thermal and mechanical analysis of batteries. It will support carmakers, equipment manufacturers and battery manufacturers in validating their products before they are put on the market.

The company points out that this facility will “support the growth of the European battery industry” and “meet the growing need for safety and performance testing” in the context of the rapid industrialisation of electric vehicles.

source : Serma

Contributing to the development of electric mobility

The work carried out at Neuville-aux-Bois is part of a series of investments designed to structure a French and European battery testing industry. The infrastructure of this new company now covers the entire life cycle of batteries: characterisation, endurance, safety, recycling and after-use expertise.

The new centre will add to the testing capacity available in France, help the industry build up its technological expertise and secure the battery value chain, a key element in Europe’s energy transition.

The year 2025 marks a major milestone for electric vehicles: almost a quarter of new cars sold worldwide are now electric. China is consolidating its dominance, while Europe is experiencing more measured growth and emerging markets such as Vietnam and Thailand are speeding up their transition. With record sales, technical innovations and a massive extension of recharging infrastructures, electromobility is emerging as a real driving force behind the global transformation of the automotive industry.

In 2025, worldwide sales of all types of electric vehicles – i.e. 100% electric and hybrid – are estimated at around 18.5 million units in the first 11 months of the year. This is a significant number: it represents growth of around 21% compared with 2024. According to industry experts, this suggests that the annual total for 2025 is likely to exceed 20 million electric cars sold.

Unsurprisingly, it is China that is massively dominating the market. Nearly 14 million electric cars were sold there this year. This represents 60% of domestic sales in the Middle Kingdom. In other words, two out of every three vehicles sold worldwide are now being driven under a Chinese banner.

The other key player in 2025 is South-East Asia. With sales of electric vehicles up by 79% in the first half of the year, according to Counterpoint Research, it is confirming its role as a driving force for soft mobility. The ASEAN region now accounts for around 5-6% of global EV sales, or more than 1 million units in the current year, compared with less than 600,000 in 2024.

Vietnam, which was already very aggressive in 2024, has seen the market share of zero-emission vehicles rise from 28% to almost 40% in just twelve months. Thailand is following the same trajectory: it now has a market share of over 20%, compared with around 12% at the end of 2024. This rapid growth can be explained by the determination of the region’s governments to structure a genuine local industrial ecosystem, combining manufacturing facilities, tax incentives and the electrification of the public fleet.

Sales, leading brands and models

In terms of volume, the BYD-Tesla duo continues to reign, but low-cost Chinese manufacturers are making their mark in almost every segment. In France, the Renault 5 E-Tech has established itself at the top of the sales charts, while the Renault brand has scored a media coup with its Filante Record prototype, capable of travelling 1,000 km on a single charge. At the top of the Asian rankings, Chery and MG are investing in solid-state batteries, promising to double their range by the end of the decade.

source : Renault

Infrastructure: the terminal challenge

In terms of infrastructure, growth remains spectacular. There will be more than 8 million public charging points worldwide by the end of 2025 (compared with 4.5 million in 2023, i.e. +78%), with China accounting for nearly 3.5 million, or 44% of the global total. Europe will have more than 1.2 million public charging points (up 40% on 2024), led by the Netherlands (183,000), France (170,000) and Germany (153,000).

According to a TrendForce projection, there will be more than 16 million public charging points on the planet by 2026.

Outlook: European realism, Asian ambition

On the legislative front, the end of the year was a turbulent one. After numerous complaints from European manufacturers, the European Union adjusted its timetable: total carbon neutrality by 2035 has been replaced by a more flexible target of -90% CO₂ emissions for new vehicles.

All over the world, electromobility is progressing, not at the same speed, but in the same direction.

In the space of just three years, however, the country has undergone a spectacular transformation. Buoyed by the emergence of its national manufacturer Togg, an extremely attractive tax system and the offensive by foreign brands, led by the US and China, Turkey is now one of the most dynamic markets on the continent.

Spectacular take-off in 2025

Turkey is experiencing impressive growth this year. In fact, while several European countries are seeing sales of electric vehicles stagnate or fall back, Turkey is breaking all the records.

Indeed, the figures speak for themselves: according to data from the Association of Automobile Distributors (ODMD), in the first eleven months of 2025, the country recorded 166,665 sales of 100% electric vehicles, more than double the figure for the same period in 2024. At this rate, Turkey is poised to end the year with an increase in sales of more than 100% in one year.

If we broaden the spectrum to electrified vehicles as a whole, the shift is even more striking. Plug-in hybrids rose by more than 658% to 42,857 units over eleven months, while conventional hybrids sold more than 252,000 units. As a result, by January-November 2025, electrified vehicles (BEV + PHEV + HEV) accounted for around 45% of total registrations, compared with less than 25% the previous year.

Togg, Tesla, BYD: a trio that dominates the market

Behind these figures, which symbolise effective progress, three brands share almost the entire 100% electric market, with radically different strategies and profiles.

The winner is Togg, Turkey’s national manufacturer. It topped the podium with 31,715 units sold over eleven months. This figure marks a symbolic turning point: for the first time, a Turkish car brand is the leader in a strategic segment. Launched in 2023 with the T10X SUV, Togg benefits from massive political support and ultra-favourable taxation reserved for locally produced models.

Credit: TOGG

Tesla came second with 29,955 sales. June was a historic month for the brand, with more than 7,200 units sold in a single month. The American brand benefited from the shortcomings of the Turkish tax system. If an EV has a power output of more than 160 kW, it is taxed heavily (40-60%). Tesla has therefore limited its vehicles to this limit to enable Turks to buy without breaking the bank.

BYD completes the podium with 17,639 units sold. A latecomer to the Turkish market at the end of 2023, the Chinese giant has methodically rolled out a range of nine models covering all segments. In 2025, BYD announced a billion-dollar investment to build a production plant in Manisa, capable of producing 150,000 vehicles a year by the end of 2026. This strategic move will enable the Chinese company to get round the 40% import tariff.

A fast-expanding recharging network

The explosion in sales is logically pushing the country to speed up the roll-out of its infrastructure. And the figures show an accelerated catch-up, even if the coverage remains very uneven.

In June 2025, Turkey had 31,433 public charging points, according to the Energy Market Regulatory Authority (EPDK), compared with just 6,500 in March 2023. This growth of more than 370% in two years reflects a real effort, albeit from a very low base. By autumn 2025, the network will have more than 37,000 outlets, concentrated in Istanbul (more than 3,000 stations), Ankara (1,322 stations) and Izmir.

Turkey’s infrastructure is structured around several major operators:

ZES dominates the market with a national network covering motorways and urban centres.

Trugo, Togg’s proprietary network, now has more than 1,000 ultra-fast DC chargers and 600 AC stations spread across the country’s 81 provinces.

Eşarj, operated by Enerjisa, offers a multi-brand network accessible via mobile application.

The problem in Turkey is that beyond the metropolises, things are more complicated. Indeed, rural areas remain largely under-equipped. Government targets are ambitious: 143,000 plugs by 2030 and 273,000 by 2035 to support an estimated 1.5 million electric vehicles. To achieve this, however, between €500 and €600 million will have to be invested.

ÖTV tax

This success does not come from nowhere. If Turkey is experiencing such an explosion in electric vehicle sales, it is above all thanks to an ultra-aggressive tax policy that makes electric vehicles the most economically rational option.

At the heart of the system is the special consumption tax (ÖTV), which applies to all new vehicles according to a scale based on power, price and origin of the vehicle. For internal combustion vehicles, this tax varies between 80% and 220% of the base price, making the purchase of a petrol or diesel car extremely expensive for the average consumer.

By contrast, electric vehicles benefit from spectacular tax reductions: 10% for models with less than 160 kW and a base price of less than 1.65 million Turkish lira (around €47,000), and up to 60% above these thresholds. Even in the most unfavourable case, an electric vehicle is still more attractive from a tax point of view than its internal combustion equivalent.

As a further government incentive, the system includes an incentive for local production: electric vehicles assembled in Turkey, such as Togg, benefit from additional tax advantages, including corporate tax deductions for the companies that buy them. This mechanism is clearly designed to favour Togg over imports.

The scheme had an immediate effect on purchasing behaviour. In June 2025, just before the tax thresholds were adjusted, sales of electric vehicles soared by 233.6% year-on-year, as buyers rushed to take advantage of the lowest rates before they were revised. Tesla, with its Model Y limited to 160 kW, made the most of this window of opportunity.

But this tax policy raises questions. By creating a massive tax advantage for Togg, the Turkish government is distorting competition and potentially discouraging other international manufacturers from investing in the country.

Ambitious targets for 2030

The Turkish government is making no secret of its ambitions. The national plan aims to have 2.5 million electric vehicles on the road by 2030, 35% of them locally produced. This target rises to 10 million vehicles by 2040, with a 100% electric fleet by 2053 to achieve carbon neutrality.

To achieve this, the government is mobilising several levers: subsidies for R&D, support for battery factories, development of the recharging network via public-private partnerships, and maintaining a tax system that favours locally produced electric vehicles.

But these objectives presuppose economic stability and a sustained growth trajectory, which the country is struggling to guarantee. High inflation, the volatility of the Turkish lira and regional geopolitical tensions are all uncertainties that could slow or compromise these ambitions.

A structuring local ecosystem

The country is gradually developing a local industrial ecosystem around electromobility.

SIRO produces batteries for Togg vehicles at its Gemlik plant. With a current capacity of 3 GWh per year, the plant aims to reach 20 GWh by 2031, enough to equip several hundred thousand vehicles.

Aspilsan produces around 22 million battery cells a year, mainly in nickel-metal-hydride and lithium-ion technologies. Historically focused on the defence and energy sectors, the company is now turning its attention to the automotive industry.

In 2025, three new battery plants came on stream: Ottomotive (5 GWh of battery packs), Reap Battery (5 GWh for energy storage) and Maxxen (10 GWh). These combined capacities of 20 GWh position Turkey as a potential regional hub for battery production.

Finally, the electric vehicle components and equipment industry is showing impressive growth: exports of spare parts for EVs reached more than €1 billion in June 2025, up 13% year-on-year.

Structural barriers to mass adoption

Despite the spectacular growth in sales, a number of obstacles remain that could slow the momentum in the medium term.

Customs tariffs, set at 40% on electric vehicles imported from China, heavily penalise buyers and limit access to the most affordable Chinese models. This protectionist measure aims to encourage local production, but it also reduces competition and keeps prices high for a large proportion of the population.

In Turkey, there are no CO₂ standards. This leaves the combustion market to flourish without regulatory pressure. Unlike the European Union, where emissions quotas force manufacturers to electrify their ranges, Turkey imposes no climate constraints on new vehicle sales.

The electricity grid is a growing concern. With a heavy reliance on imported natural gas and limited domestic renewable generation capacity, the country could face stresses on the grid if the electric vehicle fleet reaches its target of 2.5 million units by 2030.

Rural infrastructure remains largely inadequate. While the major cities account for the bulk of charging points, the rest of the country is struggling to keep up. The lack of a complete motorway network is holding back adoption for inter-city journeys.

As everywhere else, price is still an adoption issue. Even with tax benefits, an electric vehicle remains a considerable investment in a country where purchasing power is under pressure.

A European surprise, but still fragile

Turkey is emerging as one of the major surprises on the world electromobility scene. In the space of just three years, the country has gone from an anecdotal market to a player that rivals European nations.

This acceleration is largely based on a tax policy that massively favours local production to the detriment of international competition. While this strategy has made it possible to structure a national industry, it has also made the market extremely dependent on the State’s tax choices. Any downward revision of ÖTV benefits could brutally break the momentum.

Turkey is developing its electromobility, and fast. As a bridge between Europe and Asia, Turkey is ambitious. Let’s see if this transition will last over time.